The explosive growth of artificial intelligence, the outsized influence of mega-cap stocks, and the relentless surge of momentum-driven investing continues to dominate market headlines. This environment has fueled a remarkable run for a handful of large companies, leaving high-quality businesses—those with strong balance sheets, consistent profitability, and durable competitive advantages—lagging.

Yet history suggests that such phases of concentrated market leadership and speculative rallies rarely last forever. We believe the current market environment, where quality investing is out of favor, may be setting the stage for potential opportunities. As many investors continue to chase the latest trends, we maintain that the overlooked segment of quality companies could be poised for a resurgence when fundamentals reassert themselves.

What We Believe “Quality” Really Means in Today’s Market

At Kayne Anderson Rudnick, we define “quality businesses” as possessing certain traits such as:

- Strong returns on capital

- A durable business model

- A conservative balance sheet

We maintain that quality companies can self-fund growth, maintain high profitability, and keep financial leverage low, which makes them resilient, especially when economic conditions tighten.

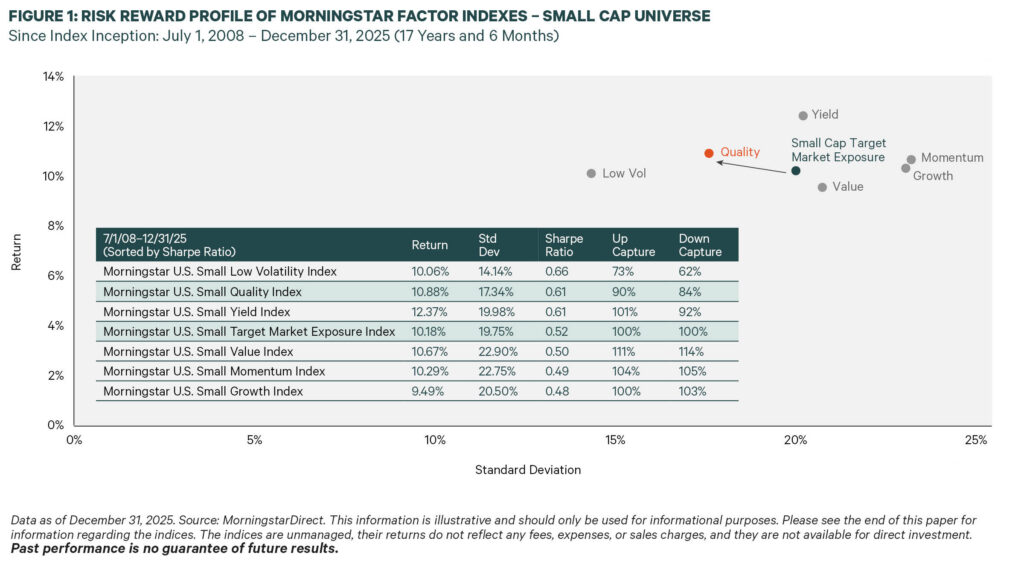

When interest rates are high, there’s less room for error: Weaker businesses with heavy debt or inconsistent earnings face greater risks. History shows that when markets shift focus back to fundamentals, quality companies tend to outperform, offering the potential for better downside protection and more consistent long-term returns (See Fig. 1).

The AI Boom: Opportunity or Risk?

The AI boom has unleashed a wave of investment and optimism, with leading technology giants projected to spend over $350 billion on AI infrastructure in 2025 alone. However, we believe this surge in capital outlays is outpacing the industry’s ability to monetize AI, as current revenues remain a fraction of companies’ spending.

And while markets are already pricing in the expectation of long-term, transformative success for AI and rewarding companies at the center of this trend with elevated valuations, history offers a note of caution: Previous infrastructure booms, such as those during the early internet era, did not guarantee lasting rewards for every early leader.

The takeaway? The gap between investment and realized earnings highlights the risk that not all current AI frontrunners will ultimately benefit as much as markets anticipate.

The Overlooked Opportunity in Small Caps

Investors often unfairly associate small-cap stocks with lower quality, but this perception originates from broad market indexes that include many unprofitable or highly leveraged companies. In reality, investing in high quality small caps may present a compelling and overlooked opportunity:

- They operate in niche markets: Many high-quality small caps stand out in specialized areas where they can build durable competitive advantages.

- They have less analyst coverage: With fewer eyes on them, these companies are more likely to be mispriced, creating opportunities for diligent investors.

- They are mispriced more often: The combination of limited coverage and index dilution means that even strong businesses can trade at attractive valuations.

In our view, this is where active selection can add the most value—by identifying resilient, well-managed small caps that are hidden beneath the surface of broad indexes. We believe disciplined, highly focused, quality investing in the small-cap universe has the potential to uncover businesses with strong returns on equity, lower debt, and more consistent earnings growth than the average index constituent.

When Momentum Leads, Quality Gets Left Behind

Today’s markets are favoring lower-quality, high-beta stocks, leaving quality names behind—a pattern that’s both familiar and cyclical. These momentum-driven phases often pull forward returns rather than sustain them, with history repeatedly demonstrating that such rallies tend to be short-lived before fundamentals regain importance.

When Underperformance Becomes the Setup

We maintain that periods when quality investing strategies fall out of favor can create attractive entry points for investors, setting the stage for a subsequent recovery as fundamentals reassert themselves. Here’s why:

● Periods of lagging performance have historically preceded rebounds, with substantially larger three- and five-year forward returns.

● Quality does not need to “catch up”; rather, financially durable, high-quality businesses require time to compound value over full market cycles and drive sustained recoveries.

● Quality investing offers opportunities when market leadership shifts back toward underlying fundamentals, creating the potential for producing favorable relative outcomes over the long term.

Why This Cycle May Be Creating a Bigger Opportunity

We believe the current market cycle presents a unique opportunity for active, quality-focused investment management, driven by a combination of structural shifts and current market dynamics:

- Fewer public companies: The number of U.S. listed companies has declined from a high of 7,000 to less than 4,000 over the past few decades due to factors like M&A and companies staying private longer.

- More dispersion in quality: The Russell 2000 Index contains a broad mix, including a substantial number of companies with lower profitability, higher leverage, or inconsistent earnings.

- Heavy concentration in large-cap returns: The S&P 500 has outperformed its equal-weighted index by the largest amount since the internet bubble, indicating that performance is concentrated in the largest companies.

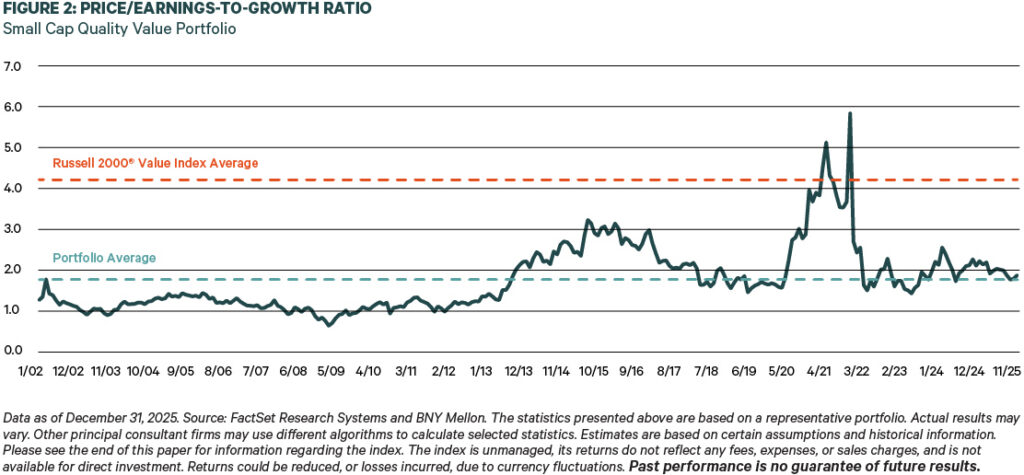

We believe that these conditions create opportunity for disciplined investors. The valuation of small-cap companies relative to large-caps has swung to a discount greater than one standard deviation, suggesting the gap between price and fundamentals may be widening (See Fig. 2).

The Bottom Line: Don’t Confuse Noise with Opportunity

Markets are currently rewarding momentum, leverage, and cyclicality, which can lead to “junk rallies” and strong short-term returns. However, history suggests that these speculative periods are short-lived, while long-term outcomes are still fundamentally driven by the consistent performance and downside protection offered by high-quality businesses.

The current increase in investor interest in lower-quality companies and the resultant performance differential in momentum stocks against quality stocks have historically presented ideal entry points for long-term quality investors. What the market is rewarding today should not be confused with long-term opportunity.

Want the full analysis behind these trends? Dive into the complete white paper for deeper data and insights.

This information is being provided by Kayne Anderson Rudnick Investment Management, LLC (“KAR”) for illustrative purposes only. Information in this article is not intended by KAR to be interpreted as investment advice, a recommendation or solicitation to purchase securities, or a recommendation of a particular course of action and has not been updated since the date listed on the correspondence, and KAR does not undertake to update the information presented. This information is based on KAR’s opinions at the time of publication of this material and are subject to change based on market activity. There is no guarantee that any forecasts made will come to pass. KAR makes no warranty as to the accuracy or reliability of the information contained herein. Past performance is no guarantee of future results.