We’ve all heard stories about how someone made a substantial profit in the market by buying and selling some stock at just the right time. However, that’s a lot like hearing about someone striking it rich at the tables in Vegas. Did they also tell you about the numerous trips they made to the tables and lost? Or did you hear about all the short-term trades that the investor made that were not nearly as successful?

What is Market Timing?

Market timing is buying and selling a stock based on predicting when the stock’s price will be low and when it will be high in the hopes that one will reap a significant return. However, nobody can accurately predict the trajectory of an individual stock. No one has a crystal ball or a fool-proof method.

To be clear, market timing depends largely on luck, and most of us know how undependable that can be.

Why Time in the Market Beats Timing the Market

Unlike trying to time the market, spending time in the market — in other words, investing for the long term — has shown consistent success. While the market does move up and down, historical data shows that the positive years far outweigh the negative years.

Despite a roller coaster ride, the stock market has increased in value — over the past 10, 20, and 30 years. For example, between 2001 and 2020, the average annualized return of the S&P 500® Index was 7.47%1.

If you were investing in 2008, you might remember that the S&P 500 lost a jaw-dropping 37% of its value that year. And yet, over the decade, investing was still profitable.

In the four years following 2008, the S&P 500® saw increases of 26%, 15%, 2%, and 16%, erasing those recession losses and leading into many more bullish years.

Historical results are not a guarantee of future results, but they do bear consideration. There are good reasons why time in the market tends to beat market timing. Some of these reasons are economical, but the most compelling reasons are connected to human behavior.

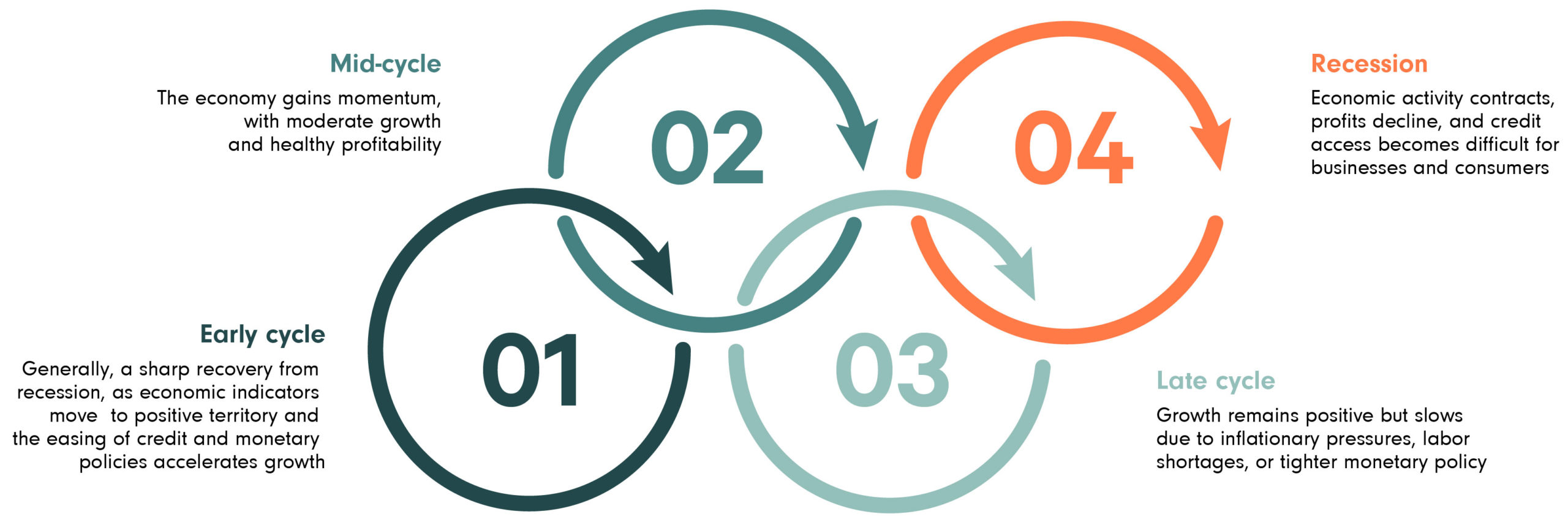

How Business Cycles Play a Role in the Market

Every business cycle is different, but certain patterns have tended to repeat over time. A typical business cycle contains four distinct phases:

Corporate earnings, interest rates, inflation, and other factors that change as economies expand and contract affect the performance of most sectors of the stock market. Further, the overall business cycle’s rise and fall is complicated by the business and growth cycles of industries and individual companies.

Each stage’s length of time in the business cycle is rarely predictable, and unforeseen economic, political or environmental events can disrupt a trend. For example, the COVID-19 pandemic ended the longest growth cycle (128 months) in U.S. history since WWII2.

In our view, the unpredictable nature of each of these business cycles is just another reason why time in the market typically beats out timing the market.

Human Behavior — Sometimes Irrational, Nearly Always Irrational

If stock prices were truly determined by the economy’s underlying fundamentals or even the specific company, predictions might be possible with some degree of accuracy. In fact, over the long-term, these factors usually win out. Stock analysts put a great deal of work into anticipating a specific company’s future success, and this research and evaluation is very useful.

However, predictions are not always accurate in the short-term because stock prices are often determined by what investors are willing to pay for the stock, and investors are human. Behavioral psychology applied to investing has uncovered several biases that show we all tend to act based on feeling rather than fact.

A study3 by H. Kent Baker and Victor Ricciardi, for example, uncovered eight biases in investor behavior:

- Confirmation bias — As humans, we tend to look for information that supports ideas we already have, right or wrong.

- Loss aversion bias — We feel losses more keenly than gains, affecting our risk-taking behavior. We might delay selling losing investments to avoid the loss.

- Disposition effect bias — We label stocks as winners or losers and treat them that way even when the tide turns.

- Hindsight bias — We believe that we can understand the past and therefore predict the future.

- Familiarity bias — We prefer investments with which we are familiar.

- Self-attribution bias — We believe we are responsible for our successes, but our failures are due to outside, single-event influences.

- Trend-chasing bias — This is why you so often hear the phrase “historical returns do not predict future investment performance.” We tend to believe they do.

- Worry — No explanation needed.

Now consider that short-term stock price movements (both up and down) are significantly influenced by human investors who are prone to these biases to varying extents.

When it comes to the matter of ‘time in the market vs timing the market,’ one can see how investor biases might come into play. It’s also precisely why we believe you should be aware of the noise in the stock market when applying a long-term investment strategy.

Patience and Clear Goals — A Recognized Strategy

We believe the best approach to investing for future goals is to be very clear about those goals, understand the time horizon needed to achieve those goals, and the amount of risk you are willing and able to take to meet them.

While short-term predictions in an attempt to time the market can sometimes be lucky, volatility and human behavior often trumps luck.

In our experience, patient investors who spend time in the market have the potential for greater profits by allowing their investments to grow steadily over time.

For personal investing guidance from our team of wealth management advisors, contact us today.

1 Data as of December 31, 2020. Data is obtained from FactSet Research Systems and is assumed to be reliable. This information is being provided by Kayne Anderson Rudnick Investment Management, LLC (“KAR”) for illustrative purposes only. Please see important disclosures below. Past performance is no guarantee of future results.

2 June 12, 2020. Pandemic Ends Longest Growth Cycle in U.S. History. Statista https://www.statista.com/chart/18513/length-of-us-expansions/

3 June 23, 2014. How Biases Affect Investor Behavior. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2457425

The S&P 500® Index is a market capitalization-weighted index which includes 500 of the largest companies in leading industries of the U.S. economy. The S&P 500 Index is not actively managed and does not reflect the deduction of any investment management or other fees and expenses. Indices are not available for direct investment. This report is based on the assumptions and analysis made and believed to be reasonable by the Advisor. However, no assurance can be given that Advisor’s opinions or expectations will be correct. This information is being provided by Kayne Anderson Rudnick Investment Management, LLC (“KAR”) for illustrative purposes only. and should not be considered a recommendation or solicitation to purchase securities and has not been updated since the publication date of the material, and KAR does not undertake to update the information presented should it change. This information is based on KAR’s opinions at the time of publication and are subject to change based on market activity. There is no guarantee that any forecasts made will come to pass. KAR makes no warranty as to the accuracy or reliability of the information contained herein. Past performance is no guarantee of future results.