Deciding when you should claim Social Security is easily one of the more complicated questions of retirement planning. While Social Security benefits may be claimed as early as age 62 for those who qualify, most people receive more over time by waiting. But how do you know whether delaying your benefits or taking them early is right for you? Here are some tips for establishing your own Social Security strategy.

Understanding Your Full Retirement Age (FRA)

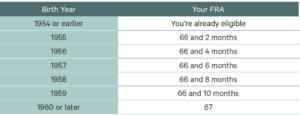

To decide when to start taking your benefits, you first need to understand your full retirement age, or FRA, for Social Security. Once you hit that FRA threshold, you’re eligible to receive 100% of your Social Security benefit.

Your FRA will depend on your birth year:

- If you were born in 1960 or later, your FRA is 67.

- If you were born in 1955 through 1959, your full retirement age for Social Security will be between 66 and two months and 66 and 10 months.

- If you were born before 1955, you’ve already reached your FRA.

Here’s a simple table to help you determine your Social Security benefits age:

Claiming Benefits Early vs. Delaying

You can claim Social Security benefits as early as age 62, before reaching full retirement age, but it’s important to understand that doing so will permanently reduce your monthly benefit. You can also choose to delay when you claim Social Security benefits. Here’s what you need to know about each approach.

Early Benefits (62+)

If you opt to start receiving Social Security benefits early, meaning before your FRA, your monthly payout will be permanently reduced. This is because benefits are adjusted based on how early you claim relative to your FRA. The reduction depends on the number of months you claim before reaching FRA. According to the Social Security Administration:

- If you claim at 62 with an FRA of 67, you’ll likely see about a 30% monthly payment reduction.

- If you claim at 62 with an FRA of 66, you’ll have about a 25% reduction in monthly payout.

In some cases, claiming early may be necessary due to health concerns, the need to cover living expenses in retirement, job loss, or debt obligations, even if it means receiving a reduced payment. Before claiming early benefits, keep in mind that this reduced monthly amount becomes your monthly payment for life aside from cost-of-living adjustments, making the timing of your claim an important factor in long-term retirement income planning.

Delayed Benefits (FRA–70)

Alternatively, delaying when you claim your Social Security benefits can also affect the amount you receive. If you delay claiming benefits beyond your FRA and up to age 70, you can earn delayed retirement credits (DRCs). These credits increase your monthly benefit by approximately 8% for each year you wait beyond FRA. For example, if your FRA is 66 and you delay claiming until age 68, you’ll see a 16% increase in your monthly benefit for the rest of your life. Delayed retirement credits stop accruing at age 70, after which there is no additional increase for waiting to claim.

Key Factors to Consider When Timing Your Benefits

While trying to figure out when you should claim Social Security, you’ll want to consider a few points based on your financial picture, health, spouse or dependents, and employment status.

1. Cash Flow & Investment Resources

Claiming Social Security benefits early may make sense if employment changes or near-term cash-flow needs affect your retirement timeline. Conversely, if you’ve retired early and have secure income from an investment portfolio, pension, or other sources, it may be beneficial to delay claiming until reaching full retirement age or later to increase your monthly benefit.

2. Life Expectancy & Health

If you have health issues, can’t work, or do not expect to live an average life, claiming Social Security early may make sense if you’re eligible. Doing so will certainly reduce your benefits, but you’ll also receive those monthly payments longer. Of course, if you’re in good health and in solid financial standing, then delaying could maximize your Social Security benefit because your monthly check will be larger.

3. Spousal Benefits & Marital Considerations

Marital status can also affect when and how you claim your Social Security benefits. Depending on your circumstances, you may be eligible to claim benefits based on your own work record or a spouse’s. In general, waiting until full retirement age can provide more flexibility and higher benefits, particularly when one spouse earned significantly more over their career. In those cases, coordinating timing may help maximize household income and provide greater financial security for the surviving spouse.

Survivor benefits may also be available to current or former spouses, as well as certain dependent or disabled family members. Because these rules vary by situation, coordinating benefits and timing is an important part of an overall retirement planning strategy.

4. Employment Income Impact

If you plan to continue working beyond age 62 or decide to go back to work after retiring, this can also have an impact on your Social Security strategy. If you claim Social Security benefits before your FRA and continue working, your benefits can be temporarily reduced if your earnings exceed an annual limit. In 2026, the earnings limit for people under FRA is $24,480, and Social Security withholds $1 in benefits for every $2 you earn above that amount. Once you reach full retirement age for Social Security, you can earn as much as you want without reducing your benefit.

Social Security Taxation and Planning

Another factor to consider when deciding whether to delay your benefit, particularly if you are still working, is taxation of Social Security. While it’s best to seek the advice of your tax professional and financial planner, you may want to postpone claiming your benefit until you reach your FRA or until your income is less than the annual limit.

Taxable Income Thresholds

Up to 50% of your Social Security benefits may be subject to federal income tax if your other income plus half of your Social Security benefits exceed certain thresholds: $25,000 annually for an individual and $32,000 for a married couple filing jointly. At higher income levels, up to 85% of Social Security benefits may be taxable.

Table Sources:

- https://www.ssa.gov/faqs/en/questions/KA-02471.html

- https://www.irs.gov/newsroom/irs-reminds-taxpayers-their-social-security-benefits-may-be-taxable

- https://www.ssa.gov/oact/progdata/taxbenefits.html

Interaction With Other Income

Social Security benefits don’t exist in a vacuum. Other income streams can directly affect how much of your benefit you owe in taxes. Portfolio income such as dividends, interest, and capital gains, along with withdrawals from traditional IRAs and 401(k)s, count toward your combined income. Pension payments factor in as well.

Tax-Planning Strategies

As these income sources increase, they can push you past key IRS thresholds and trigger taxes up to 50% or, at higher income levels, up to 85% of your Social Security benefits. Coordinating when and how you take income from investments, retirement accounts, and pensions therefore plays a meaningful role in managing the taxation of Social Security and your overall tax burden in retirement. Effective tax planning includes timing distributions to help reduce taxable benefits, aligning income with Roth conversions or withdrawals from tax-deferred accounts, and managing provisional income to help minimize IRMAA-related (income-related monthly adjustment amount) Medicare surcharges.

Social Security as Retirement Insurance

Waiting at least until your full Social Security benefits age may be beneficial over the long run, particularly if you’re in good health, but you should not delay benefits past age 70. A longer-than-expected retirement, inflation, and market volatility pose the biggest risks to claiming Social Security early. When these risks match your concerns, delaying Social Security can help you establish a reliable form of protection for the future.

Treat Social Security as your retirement insurance and a guaranteed income floor—one that helps protect against longevity risk, market swings, and rising costs. By delaying when you claim your Social Security benefits, you may be able to strengthen a stable, predictable income source that can anchor your retirement plan and support you no matter how long you live or how markets perform.

The Importance of Individual Financial Planning

Deciding when to claim Social Security is an important part of retirement planning. Working with an experienced financial planner and tax professional can help you understand how your income, investments, expenses, taxes, and health considerations may affect your benefits. Contact your KAR wealth advisor to discuss how Social Security and Medicare planning can fit into your broader financial plan.

This information is being provided by Kayne Anderson Rudnick Investment Management, LLC (“KAR”) for illustrative purposes only and should only be used for informational purposes. The information provided here should not be considered legal or tax advice and all investors should consult their legal and/or tax professional about the specifics of their own legal and tax situation to determine any proper course of action for them. KAR does not provide legal or tax advice and nothing herein should be construed as legal or tax advice, and information presented here may not be true or applicable for all legal and income tax situations. Tax laws can and frequently do change, and KAR does not undertake to update information this should any changes occur. Information in this article is not intended by KAR to be interpreted as investment advice, a recommendation or solicitation to purchase securities, or a recommendation of a particular course of action and has not been updated since the date listed on the report, and KAR does not undertake to update the information presented. KAR makes no warranty as to the accuracy or reliability of the information contained herein.